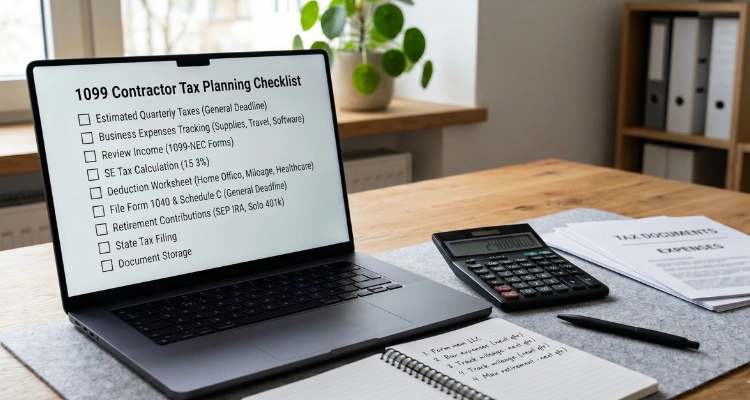

1099 Contractor Tax Planning Checklist for Self-Employed Professionals

Getting paid as a 1099 contractor can feel simple until tax planning enters the picture. The money comes in without federal withholding, without employer payroll tax support, and often without a clean month-by-month system for tracking what you earned, spent, saved, and owe.

That is why self-employed tax planning has to happen before filing season. By the time a Form 1099-NEC or 1099-K arrives, the real planning year is mostly over. The better approach is to build a checklist that runs all year, so quarterly payments, deductions, recordkeeping, and cash reserves are not handled in a rush.

For 2026, there are several updates self-employed professionals should not miss. The IRS states that self-employed individuals generally pay both income tax and self-employment tax, estimated taxes are commonly used because no employer is withholding for you, and certain 1099 reporting thresholds changed under newer federal law.

We often see contractors focus only on “how much should I save for taxes?” That question matters, but it is not enough. A strong checklist also protects deductions, confirms whether quarterly payments are required, keeps business records lender-ready, and helps you make better decisions before December 31.

Key Takeaways

- 1099 income needs active planning: Self-employed professionals usually receive income without tax withholding, so taxes must be planned during the year instead of waiting for filing season.

- Self-employment tax is separate: Contractors may owe income tax plus self-employment tax, which covers Social Security and Medicare for people who work for themselves.

- Quarterly estimates matter: Individuals, including sole proprietors and partners, generally make estimated payments if they expect to owe $1,000 or more when filing.

- Records drive deductions: A deduction is only useful if the business purpose, amount, date, and support are clear enough to defend later. 5. 1099 thresholds changed: For 2026 payments, certain federal 1099-NEC and 1099-MISC reporting thresholds increased to $2,000, but taxable income still must be reported.

- Mileage needs a log: The 2026 IRS business mileage rate is 72.5 cents per mile, but contractors need records that separate business driving from personal driving.

- Retirement planning can reduce taxable income: SEP IRAs, Solo 401(k)s, SIMPLE plans, and IRAs can create tax planning opportunities when they fit the contractor’s income and timing.

- Year-end review is essential: The best self-employed tax planning happens before the year closes, when estimated payments, deductions, retirement contributions, and entity decisions can still be adjusted.

What should every 1099 contractor do before tax season?

Every 1099 contractor should track gross income, separate business and personal expenses, estimate federal and state tax payments, document deductions, reconcile 1099 forms, and review year-end planning opportunities before December 31. The goal is not just filing a return. The goal is avoiding surprises while keeping accurate records throughout the year.

Start with the basics: a business bank account, a bookkeeping system, copies of every client payment record, and a recurring calendar reminder for quarterly tax review. For self-employed professionals, this system is your replacement for an employer payroll department.

A contractor who waits until January to reconstruct twelve months of income will usually miss something. A contractor who reconciles monthly can see profit trends, set aside tax cash, confirm deductions, and avoid guessing when estimated tax deadlines arrive.

Need a clearer system for your 1099 income and expenses?

Checklist step 1: Confirm what counts as 1099 contractor income

1099 contractor income includes payments you receive for services as an independent contractor, freelancer, consultant, gig worker, or self-employed professional. It can arrive through client checks, ACH deposits, payment apps, marketplaces, cash payments, or platform payouts. A form helps confirm income, but it does not create the tax obligation by itself.

For 2026, one easy mistake is assuming that no form means no taxable income. That is not how reporting works. The IRS reminded gig economy workers that taxpayers must report all income when filing, regardless of whether they receive Form 1099-K or another information return.

This matters because the federal Form 1099-K threshold for third-party settlement organizations has returned to more than $20,000 and more than 200 transactions. Separately, the IRS 2026 general information return guidance says certain payment reporting thresholds increased from $600 to $2,000 for tax years beginning after 2025.

For contractors, the practical rule is simple: track every dollar you earn, whether it appears on Form 1099-NEC, Form 1099-K, a marketplace statement, a client email, or your bank deposits. The IRS form is a reconciliation tool, not your only income record.

Checklist step 2: Separate business money from personal money

A separate business bank account gives self-employed professionals a cleaner way to track income, deductions, tax reserves, and owner draws. Even if you operate as a sole proprietor, separation reduces confusion and makes monthly accounting much easier when multiple clients, platforms, or payment methods are involved.

At minimum, contractors should keep one checking account for business receipts and expenses, one savings account for tax reserves, and one bookkeeping process that categorizes transactions monthly. If you use QuickBooks or another accounting system, connect only the accounts that truly belong to the business.

This is where strong bookkeeping becomes tax planning, not just administration. Virtue Advisors supports business owners with monthly accounting services when they need cleaner records, better reporting, and a more reliable view of income before estimated tax deadlines.

Checklist step 3: Understand self-employment tax before estimating payments

Self-employment tax is the Social Security and Medicare tax paid by people who work for themselves. It is not the same as regular federal income tax. The IRS self-employment tax page states that the self-employment tax rate is 15.3%, made up of 12.4% for Social Security and 2.9% for Medicare.

For 2026, the Social Security taxable maximum is $184,500, while Medicare has no wage cap. The Social Security Administration also notes that higher earners may be subject to an additional 0.9% Medicare tax above applicable earned income thresholds.

The IRS also states that you must pay self-employment tax and file Schedule SE if your net earnings from self-employment are $400 or more. That $400 rule is based on net earnings, not simply the total amount a client paid you.

| Tax Item | What It Means for a 1099 Contractor | Planning Action |

|---|---|---|

| Gross income | All business income received before expenses. | Track every payment source monthly. |

| Net profit | Gross income minus ordinary and necessary business expenses. | Use bookkeeping to estimate taxable profit, not just bank balance. |

| Self-employment tax | Social Security and Medicare tax for people who work for themselves. | Estimate it separately from income tax. |

| Federal income tax | Tax based on taxable income, filing status, deductions, and credits. | Review year-to-date profit before each estimate. |

| State tax | Separate state obligations may apply depending on where you live or work. | Check state rules and deadlines separately. |

Note: This table is a planning summary only. Exact tax outcomes depend on filing status, deductions, credits, state rules, and business facts.

Bottom Line: Do not estimate 1099 taxes from gross receipts alone. Start with net profit, then account for both income tax and self-employment tax.

Checklist step 4: Set quarterly estimated tax review dates

Quarterly estimated tax planning helps contractors pay tax as income is earned instead of waiting until the annual return is filed. The IRS says individuals, including sole proprietors, partners, and S corporation shareholders, generally make estimated payments if they expect to owe tax of $1,000 or more when the return is filed.

For tax year 2026, Publication 505 lists the individual estimated tax due dates as April 15, 2026, June 15, 2026, September 15, 2026, and January 15, 2027. Contractors with uneven income may need to annualize income rather than simply divide the year into four equal payments.

A practical rhythm is to close your books ten days after each payment period, compare year-to-date profit against the prior estimate, and adjust before the deadline. If your income changed sharply, do not wait until year-end to fix the estimate.

Checklist step 5: Track deductions while the proof is still fresh

The best deductions are tracked when they happen. Self-employed professionals should keep receipts, invoices, mileage logs, subscription records, bank statements, and notes that explain the business purpose of each expense. Waiting months makes legitimate deductions harder to support.

Common contractor deduction categories include software, professional education, business insurance, subcontractor costs, supplies, advertising, accounting fees, payment processing fees, phone or internet business use, home office expenses, mileage, and retirement contributions. Eligibility depends on the facts, so documentation matters.

If you use a vehicle for business, the IRS 2026 optional standard mileage rate is 72.5 cents per mile for business use. The rate is optional, which means some contractors may instead use actual expenses when that method is better supported and allowed.

For home office planning, the IRS simplified option allows a standard deduction of $5 per square foot of home used for business, up to 300 square feet, but it does not change the basic eligibility criteria. The space generally must be used regularly and exclusively for qualified business use.

Checklist step 6: Reconcile every 1099 form against your own books

When tax forms arrive, compare them against your own records before filing. A 1099 may include gross payments before fees, report payments received through a platform, or reflect a client’s records differently from your bookkeeping. Do not assume the form is wrong, but do not ignore differences either.

For 2026 payments, payers may issue fewer forms because some federal reporting thresholds increased. That does not remove the contractor’s obligation to report income. It simply makes your own records more important, because your income statement may be more complete than your tax forms.

Contractors who also hire subcontractors should collect Form W-9 before paying vendors and should review whether information return filing rules apply. If you are both a contractor and a payer, your year-end checklist should include vendor cleanup before January filing deadlines.

| Checklist Area | Review Monthly | Review Quarterly | Review At Year-End |

|---|---|---|---|

| Income | Record every deposit by client or platform. | Compare actual income to estimate. | Reconcile Forms 1099 to books. |

| Expenses | Attach receipts and categorize costs. | Check whether deductions are supported. | Review large purchases and missing receipts. |

| Taxes | Move funds to tax reserve account. | Calculate and pay estimated tax if required. | Confirm safe harbor and final balance due. |

| Mileage/home office | Update mileage and space records. | Check business-use percentage. | Choose standard mileage, actual expense, or home office method with support. |

| Retirement/QBI | Monitor net profit. | Estimate contribution capacity. | Review retirement and QBI planning before filing. |

Note: The timing shown above is a practical planning rhythm, not a substitute for individualized tax advice.

Bottom Line: A tax checklist works best when it is repeated monthly and quarterly, not when it is opened for the first time in March.

Want to connect tax planning, retirement planning, and cash flow before year-end?

Checklist step 7: Review retirement contributions before the year gets away

Retirement planning can be one of the most useful tax planning areas for self-employed professionals, but the right option depends on income, employees, cash flow, deadlines, and plan rules. SEP IRAs, Solo 401(k)s, SIMPLE plans, and traditional or Roth IRAs may each fit different situations.

For 2026, the IRS announced that the 401(k) employee contribution limit increased to $24,500 and the IRA contribution limit increased to $7,500. Catch-up rules also changed, including an $8,000 catch-up limit for many participants age 50 and older in 401(k)-type plans.

The key is not simply choosing the biggest number. The key is matching the plan to your net earnings, whether you have employees, how predictable your cash flow is, and how quickly you need the plan established. Contractors should review this well before year-end, not after the return is being prepared.

Checklist step 8: Check QBI and new 2026 contractor-related changes

The qualified business income deduction can be relevant for many self-employed professionals, but it is calculation-heavy and subject to limits. The IRS describes QBI as the net amount of qualified income, gain, deduction, and loss from a qualified trade or business, and states that eligible taxpayers may deduct up to 20% of QBI.

The IRS also notes in its gig economy guidance that the QBI deduction is now permanent, allowing eligible gig workers to plan long term. That does not mean every contractor receives the full deduction; taxable income levels, service business rules, net capital gain, and other limits can affect the result.

Some contractors may also be affected by newer provisions for qualified tips, bonus depreciation, or business asset purchases. These rules can be useful, but they are not automatic. They require careful records and a clear link between the expense or income item and the eligible business activity.

Checklist step 9: Build a year-end tax planning file before December 31

A year-end planning file helps contractors avoid the most common filing-season scramble. It should include year-to-date profit and loss, balance sheet if applicable, mileage summary, home office records, contractor/vendor W-9s, loan statements, retirement contribution notes, estimated tax confirmations, and a list of major business changes.

This is also the time to ask whether your current structure still fits. A sole proprietorship may be simple, but growing profit, employees, recurring subcontractors, multi-state work, or liability concerns may make entity and payroll conversations more important. Do not change structure casually; review the tax, legal, payroll, and administrative impact first.

For contractors moving from side income to a full business, Virtue Advisors can help align tax preparation, bookkeeping, entity setup, and business tax planning so decisions are made with a full financial picture instead of isolated advice.

Why Virtue Advisors: Practical Tax Planning for Self-Employed Professionals

1099 contractor tax planning is not just about filing a Schedule C. A single contractor may need income tax planning, self-employment tax estimates, bookkeeping, entity guidance, retirement contribution planning, state tax awareness, and year-end deduction review. Those pieces work better when they are connected.

Virtue Advisors brings an advisory-first tax, accounting, valuation, and business consulting perspective to that process. With 1,100+ clients served across sectors and 100k+ service hours delivered, our team helps business owners and self-employed professionals move from reactive filing to clearer financial planning.

Across the contractors and small businesses we support, we often see the same pattern: better records create better estimates, better estimates reduce surprises, and better planning turns tax season into a review instead of a rescue mission.

Conclusion

A strong 1099 contractor tax checklist should help you answer four questions all year: what did I earn, what did I spend, what do I owe, and what should I adjust before deadlines pass? If you can answer those questions monthly, filing season becomes much easier.

For 2026, self-employed professionals should pay special attention to estimated tax requirements, self-employment tax, updated 1099 reporting thresholds, mileage records, home office support, QBI, and retirement planning. The details matter, but the system matters even more.

Virtue Advisors helps self-employed professionals turn tax questions into clear next steps.

Frequently Asked Questions